National Overview

After benefiting from a pandemic-era boost in spending and consumption, retail sector fundamentals began to waiver during the second half of 2022. Investors inched into 2023 cautiously, but several critical retail growth metrics have continued to trend positively early this year.

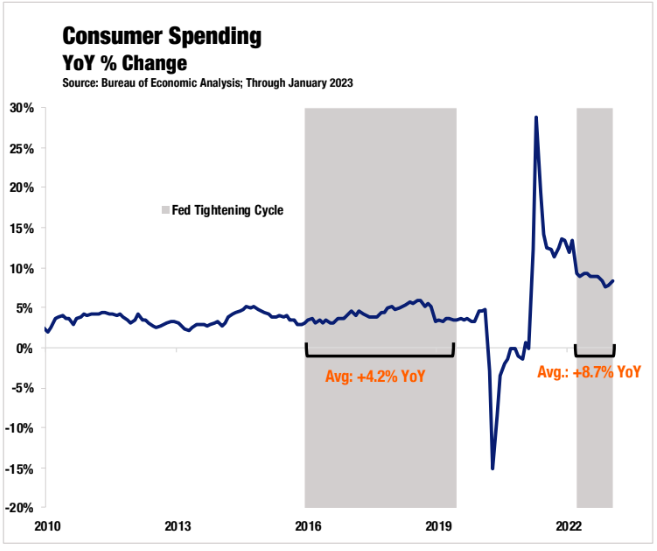

Above all, consumer spending continues to defy the damnation of inflation. According to the Bureau of Economic Analysis, personal outlays increased by $312.5 billion in January, growing by 1.8% from December and 8.4% over the last 12 months. As consumption normalizes from sky-high 2021 growth levels, it’s been tempting to view the reversion as an impending headwind for retail. Yet, if inflation’s downtrend continues without significant pain to labor markets, today’s expenditure levels may represent a new equilibrium for consumer spending.

Since monetary policy tightening began in March 2022, consumer spending has grown at an average of 8.4% year-over-year, well above the 4.2% average rate reached during the Fed’s last tightening cycle before the pandemic. Further, during the previous cycle, consumption growth did not substantially slow until COVID-19 hit US shores, and subsequent shutdowns, layoffs, and reduced spending ensued.

Overall, the retail sector continues to go through a reorganization process. At its core, retail real estate is valued by its ability to put goods and services in the hands of consumers. That requires not only a willingness to spend from consumers — but also a preference for how they interact with goods, brands, and services across a digital-physical divide. I

ncreasingly, online retailing has become an incubator of sorts, where successful brands will mature into brick-and-mortar as part of a second- stage expansion. While the US remains over-retailed and the market correction is ongoing, new models of success are emerging. It is not to say that momentum has (or will) suddenly rush in for retail. Still, more and more, it looks like the retail sector’s worst days are in the rearview.

Financials

Transaction Volume

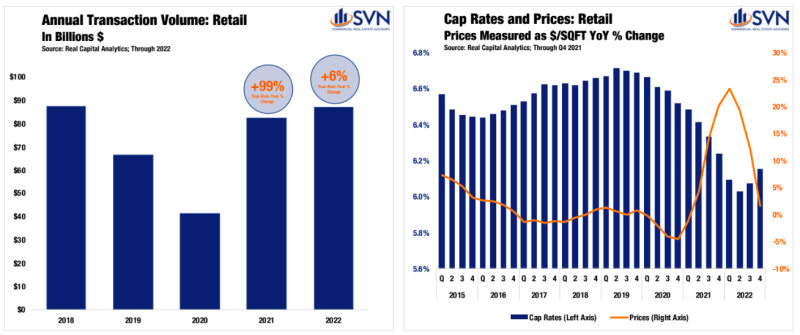

According to MSCI Real Capital analytics, retail transaction volume totaled $86.8 billion in 2022 — increasing 5.6% from the previous year. Retail was the only one of the “core four” commercial property types to see an increase last year. Often, structural forces are more impactful than cyclical ones. The retail sector was already experiencing a secular reorganization when the pandemic hit. T

hen, the exogenous shock of the shutdown and protracted period of social distancing hyper-accelerated the retail sector’s shakeout. While the process was painful, the sector is starting to see the light on the other side. A combination of the sector having less rightsizing left to do, and retailers experimenting with new hybrid models that blend e-commerce with brick-and-mortar, is fueling optimism for the sector ahead — leading to more investment. Last year marked the first time that retail investment volumes increased in consecutive years since 2015.

Cap Rates and Prices

Cap rates in the retail sector followed the trend observed throughout the rest of the commercial real estate ecosystem. As capital sought deals ahead of the Fed’s widely anticipated monetary tightening, cap rates sank to new all-time lows. For retail properties, cap rates reached their low point in Q2, touching down to 6.0%. While cap rates then started picking up in Q3 and Q4, the movements were mild compared to other property types. By the end of the year, cap rates had risen to 6.2%, though they only moved by a total of 13 basis points off their Q2 nadir.

With retail cap rates starting to inch higher, the wind in the sails of pricing has died down. Prices kept on rising through the first three quarters of the year, reaching a new all-time high of $300/sq ft in Q3.

However, reflecting the impact of higher interest rates, pricing started to soften, with retail asset valuations declining to $287/sqft. While prices remain up by 1.6% year-over-year, the drop from the previous quarter was a more substantial — 4.3% — the most significant quarter-over quarter decrease since 2009.

Regional Performance

In developing the regional retail rankings, the SVN Research Team utilized a scoring matrix. The matrix offers a comprehensive view of how regional markets are performing within the context of growth from a year earlier, as well as compared to before the pandemic. The eight following criteria were included in the matrix:

- Transaction Volume: 1-Year % Change

- Transaction Volume: % Change Over Pre-Pandemic (2019)

- Share of US Transaction Activity: 1-Year Change

- Share of US Transaction Activity: Change Since Pre-Pandemic

- Cap Rates: 1-Year Change

- Cap Rates: Change Since Pre-Pandemic

- Pricing: 1-Year % Change

- Pricing: % Change Over Pre-Pandemic

Top Performers: Southeast

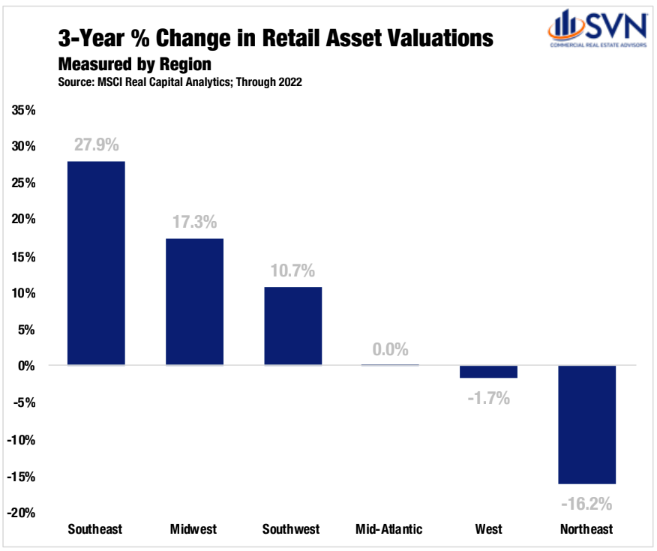

Shockingly, it turns out that attracting many new residents (who also happen to be consumers) into your region is a good thing for retail, too. The Southeast, a hotspot destination for young, starting-out families priced out of affordable housing options in high-cost markets, has seen broad commercial real estate success.

Over the past three years, retail asset prices have soared in the Southeast by 27.9% — blowing past every other corner of the country. The pricing increase comes with more investment dollars targeting retail assets.

All regions saw a rise in retail investment volume between 2019 and 2022. However, these growth rates sat between 6% and 33% for all areas other than the Southeast. Meanwhile, growth in the Southeast lapped the rest of the playing field, jumping by an incredible 75.8% in that time.