Inflation, uncertainty, tightening, recession — these are just a few of the many terms thrown around in recent months regarding the market, placing investor pessimism on display. However, the economy is sending mixed signals about its health.

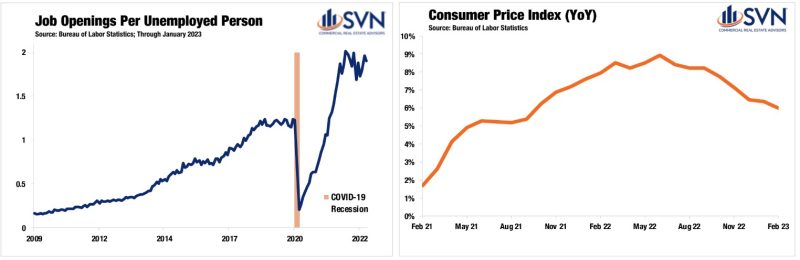

While several large and attention-generating companies have recently completed or announced rounds of layoffs, nationwide job growth continues to be relatively impressive. According to the Bureau of Labor Statistics, the US economy added 311,000 jobs in February, falling from a January tally of 504,000 but far from labor market loosening. Unemployment claims have jumped to begin March after falling to a nine-month low in January, but job openings remain robust, with more than 10.8 million open positions across the country.

However, investor jitters aren’t without merit. Over the past several weeks, a complex web of economic data, business news, and policymaker statements have only blurred the outlook further.

Let’s start with inflation. The post-pandemic inflation saga has now stretched into its third calendar year, and while there are signs that price growth is slowing, policymakers will be keen on preventing embers from reigniting the flame. After peaking at a generational high of 8.9% in June of last year, the Consumer Price Index (CPI) has improved for seven straight months, declining to a 6.0% annual inflation rate in February. Still, even if monthly inflation remained flat (0%) through the next six months, annual inflation would still be above the Fed’s 2% target.

Despite rising uncertainty, early 2023 data suggests that at least some of last year’s momentum is carrying into the new year, dampening the likelihood that we are already in recession. Still, policymakers at the Federal Reserve are warning that more good news about the economy may be increasing the risk of a hard landing. As the US economy charges forward, it risks placing further upward pressure on prices, backing the Fed into a corner where higher rates are their only tactical option.

Minutes from the FOMC’s January policy meeting alongside a March 7th speech by Fed Chair Jerome Powell reflected the committee’s willingness to again “increase the pace” of rate-hikes if, in Powell’s words, the “totality of the data were to indicate” such was needed. Fed officials’ increasingly hawkish sentiment has reinforced the consensus that policymakers will be going the distance on fighting inflation, even if markets sit in the crosshairs.

However, a new development may throw water on the Fed’s plans. On March 10th and in the days since, the collapse of Silicon Valley Bank and Signature Bank became the largest US bank failures since the 2008 financial crisis — primarily due to a lapse in strategy for today’s rising interest-rate environment. While regulators have stepped in and given public assurances to help affirm faith in the financial system, the market is betting the SVB failure forces Jerome Powell and company to pivot their monetary policy.

According to the Chicago Mercantile Exchange’s Fed Watch Tool, futures markets are pricing in a 58.3% chance of a 25-basis point hike in March and a 41.7% chance that the committee will

rates constant at 450-475 (as of the morning of March 13th, 2023).

For context, just a few weeks ago, an overwhelming majority (90.8%) of futures traders projected a 25-basis point rate increase in March, driven toward consensus by improving metrics and a gradual reduction in the Fed’s recent rate hikes. The consensus then shifted to forecasting a 50-basis point hike following Powell’s hawkish March 7th press conference — only to move back to 25 bps following the SVB failure.

Overall, the state of the US market in 2023 is, well…complicated. And we didn’t even mention Washington’s ongoing debt ceiling dilemma. As investors look through their windshields, factoring in this increased uncertainty will be necessary. Receding market panic from the SVB/Signature collapse alongside inflation’s tepid deceleration in February increases the likelihood that policymakers will raise rates by at least a 25 basis points later this month. If the above assumption holds, the development should provide markets with a better sense of direction moving forward and reduce short-term uncertainty.